28 U.S.C. §297: Assignment of judges to courts of the freely associated compact states:

TITLE 28 > PART I > CHAPTER 13 > Sec. 297.

Sec. 297. - Assignment of judges to courts of the freely associated compact states

(a) The Chief Justice or the chief judge of the United States Court of Appeals for the Ninth Circuit may assign any circuit or district judge of the Ninth Circuit, with the consent of the judge so assigned, to serve temporarily as a judge of any duly constituted court of the freely associated compact states whenever an official duly authorized by the laws of the respective compact state requests such assignment and such assignment is necessary for the proper dispatch of the business of the respective court.

(b) The Congress consents to the acceptance and retention by any judge so authorized of reimbursement from the countries referred to in subsection (a) of all necessary travel expenses, including transportation, and of subsistence, or of a reasonable per diem allowance in lieu of subsistence. The judge shall report to the Administrative Office of the United States Courts any amount received pursuant to this subsection

81A Corpus Juris Secundum (C.J.S.), United States, §29 (1999):

"Generally, the states of the Union sustain toward each other the relationship of independent sovereigns or independent foreign states, except in so far as the United States is paramount as the dominating government, and in so far as the states are bound to recognize the fraternity among sovereignties established by the federal Constitution, as by the provision requiring each state to give full faith and credit to the public acts, records, and judicial proceedings of the other states..."

[81A Corpus Juris Secundum (C.J.S.) §29, legal encyclopedia]

31 C.F.R. §515.301 Foreign Country

§ 515.301 Foreign country.The term foreign country also includes, but not by way of limitation:

(a) The state and the government of any such territory on or after the “effective date” as well as any political subdivision, agency, or instrumentality thereof or any territory, dependency, colony, protectorate, mandate, dominion, possession or place subject to the jurisdiction thereof,

(b) Any other government (including any political subdivision, agency, or instrumentality thereof) to the extent and only to the extent that such government exercises or claims to exercise control, authority, jurisdiction or sovereignty over territory which on the “effective date” constituted such foreign country,

(c) Any person to the extent that such person is, or has been, or to the extent that there is reasonable cause to believe that such person is, or has been, since the “effective date,” acting or purporting to act directly or indirectly for the benefit or on behalf of any of the foregoing, and

(d) Any territory which on or since the “effective date” is controlled or occupied by the military, naval or police forces or other authority of such foreign country.

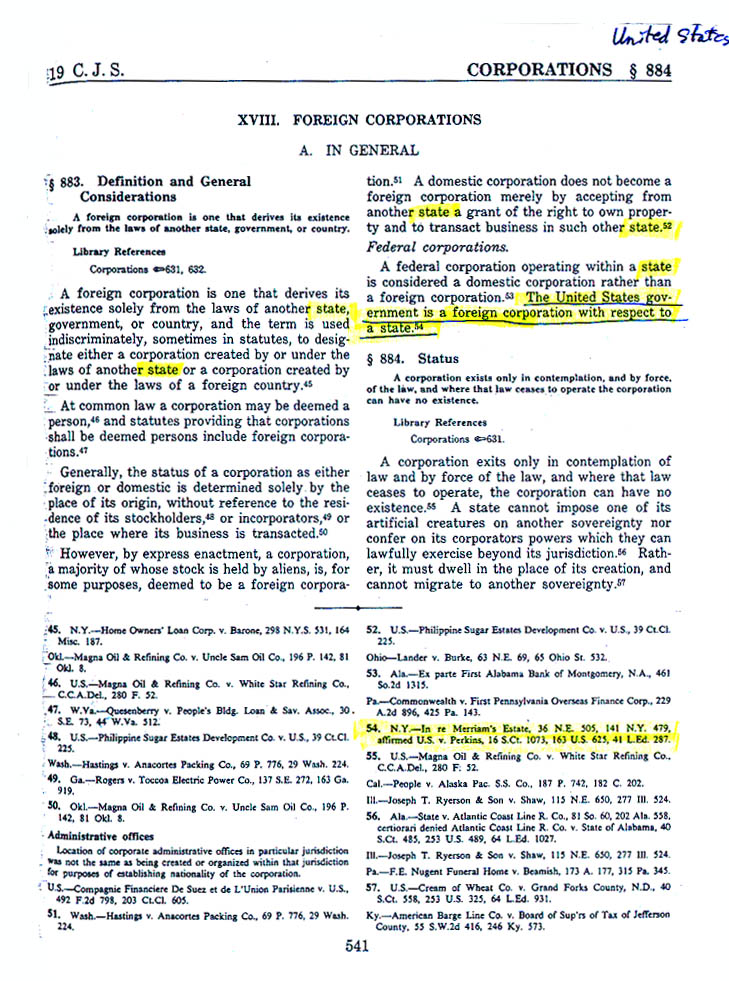

19 Corpus Juris Secundum (C.J.S.), Corporations, §884:

{kind=link}

“The United States Government is a foreign corporation with respect to a state.” [N.Y. v. re Merriam 36 N.E. 505; 141 N.Y. 479; affirmed 16 S.Ct. 1073; 41 L. Ed. 287] [underlines added]

IRS Publication 54: Foreign Country

The term “foreign country” doesn’t include Antarctica or U.S. possessions such as Puerto Rico, Guam, the Commonwealth of the Northern Mariana Islands, the U.S. Virgin Islands, and Johnston Island. For purposes of the foreign earned income exclusion, the foreign housing exclusion, and the foreign housing deduction, the terms “foreign,” “abroad,” and “overseas” refer to areas outside the United States and those areas listed or described in the previous sentence.

[IRS Publication 54, 2023, p. 17; SOURCE: https://www.irs.gov/pub/irs-prior/p54--2023.pdf]

36A Corpus Juris Secundum (C.J.S.), Foreign, pp. 1092-1093 (224 Kbytes)

36A Corpus Juris Secundum (C.J.S.), Foreign, pp. 1092-1093 (224 Kbytes)

Black's Law Dictionary, Sixth Edition, p. 498:

Dual citizenship. Citizenship in two different countries. Status of citizens of United States who reside within a state; i.e., person who are born or naturalized in the U.S. are citizens of the U.S. and the state wherein they reside.

[Black's Law Dictionary, Sixth Edition, page 498]

IRS Publication 519: Tax Guide for Aliens, Year 2007, p. 15

Foreign country. The term "foreign country" means any territory under the sovereignty of a government other than that of the United States. The term also includes territorial waters of the foreign country, the airspace over the foreign country, and the seabed and subsoil of submarine areas adjacent to the territorial waters of the foreign country.

[

California Revenue and Taxation Code, Section 17019:

17017. "United States," when used in a geographical sense, includes the states, the District of Columbia, and the possessions of the United States.

17019. "Foreign country" means any jurisdiction other than one embraced within the United States.

26 C.F.R. §301.7701(b)-2

26 C.F.R. §301.7701(b)-2

(b) Foreign country.

For purposes of section 7701(b) [26 USCS § 7701(b)] and the regulations thereunder, the term “foreign country” when used in a geographical sense includes any territory under the sovereignty of the United Nations or a government other than that of the United States. It includes the territorial waters of the foreign country (determined in accordance with the laws of the United States), and the seabed and subsoil of those submarine areas which are adjacent to the territorial waters of the foreign country and over which the foreign country has exclusive rights, in accordance with international law, with respect to the exploration and exploitation of natural resources. It also includes the possessions and territories of the United States.

(c) Tax home —

(1) Definition.

For purposes of section 7701 (b) [26 USCS § 7701(b) and the regulations under that section, the term “tax home” has the same meaning that it has for purposes of section 162(a)(2) [26 USCS § 162(a)(2)] (relating to travel expenses while away from home). Thus, an individual’s tax home is considered to be located at the individual’s regular or principal (if more than one regular) place of business. If the individual has no regular or principal place of business because of the nature of the business, or because the individual is not engaged in carrying on any trade or business within the meaning of section 162(a) [26 USCS § 162(a)], then the individual’s tax home is the individual’s regular place of abode in a real and substantial sense.

(2) Duration and nature of tax home.

The tax home maintained by the alien individual must be in existence for the entire current year. The tax home must be located in the same foreign country for which the individual is claiming to have the closer connection described in paragraph (d) of this section.

[EDITORIAL: "tax home" is the domicile of the OFFICE established by taking "trade or business" deductions. That office is domiciled in the District of Columbia per 4 U.S.C. 72. Notice also that "possessions and territories" are "foreign countries", just like states of the Union.]

26 C.F.R. §1.911-2(h):

The term "foreign country" when used in a geographical sense includes any territory under the sovereignty of a government other than that of the United States**. It includes the territorial waters of the foreign country (determined in accordance with the laws of the United States**), the air space over the foreign country, and the seabed and subsoil of those submarine areas which are adjacent to the territorial waters of the foreign country and over which the foreign country has exclusive rights, in accordance with international law, with respect to the exploration and exploitation of natural resources.

______________________

EDITORIAL NOTE: If the above regulation were to be interpreted any way other than that intended by the U.S. Constitution, the sovereign jurisdiction of the federal government would be in conflict with the sovereign jurisdiction of the 50 States of the union. In other words, such an interpretation would be illogical and have absurd consequences. Sovereignty over territory is therefore the key. There simply cannot be two sovereign governmental authorities over a territory because a territory can have only one owner. Sovereignty is the authority to which there is no political superior inside a territory. Sovereignty is vested in one or the other sovereign entity over a given territory, such as a state or the federal government, but not both entities simultaneously. The 50 union states ARE NOT territories of the federal government. They CREATED the federal government and the CREATION cannot be superior to the CREATOR. See Great IRS Hoax, section 4.1 for further explanation on this subject of the order of creation and the hierarchy of sovereignty that results from it, which we call "Natural Order".

“A State does not owe its origin to the Government of the United States, in the highest or in any of its branches. It was in existence before it. It derives its authority from the same pure and sacred source as itself: The voluntary and deliberate choice of the people…A State is altogether exempt from the jurisdiction of the Courts of the United States, or from any other exterior authority, unless in the special instances when the general Government has power derived from the Constitution itself.”

[Chisholm v. Georgia, 2 Dall. (U.S.) 419 (Dall.) (1794)]See also Arnett v. Comm'r, 473 F.3d. 790(2007) for caselaw on this subject.