Internal Revenue Service Website

IRS Employees

Paid by the Dept of Agriculture, NOT the Dept of Treasury

IRS Employees

Paid by the Dept of Agriculture, NOT the Dept of Treasury

Revenue Act of 1939, First Version of Internal Revenue Code

53 State 489

Revenue Act of 1939

Chapter 43: Internal Revenue Agents

Section 4000 Appointment

The Commissioner may, whenever in his judgment the necessities of the service so require, employ competent agents, who shall be known and designated as internal revenue agents, and, except as provided for in this title, no general or special agent or inspector of the Treasury Department in connection with internal revenue, by whatever designation he may be known, shall be appointed, commissioned, or employed.

Origins and

Authority of the Internal Revenue Service, Form #05.043 (OFFSITE

LINK)-proves that the IRS is not part of the government and has NO LEGISLATIVE

AUTHORITY to even exist.

SEDM Forms page

The Work and Jurisdiction of the Bureau of Internal Revenue-detailed

history of the IRS

Administrative

History of the IRS-Declassified document published by the IRS

Dept. of Justice Admits Under Oath that the IRS is NOT an Agency of the Federal Government

Officers of the

United States Within the Meaning of the Appointments Clause,

U.S. Attorney Memorandum Opinion-describes legal criteria for

deciding whether someont is an "officer" of the United States.

IRS employees don't meet this criteria

37 Fed.Register 20960-20964, 1972: History of the IRS

History of Treasury Department Organization

Tax History Website-detailed history of taxes in America

75 Years

of Criminal Investigation History: 1919-1994-IRS

Treasury Inspector General Audit Reports of the IRS

IRS Restructuring and Reform Act of 1998

5 U.S.C. §105: Executive Agency

TITLE 5--GOVERNMENT ORGANIZATION AND EMPLOYEES PART I--THE AGENCIES GENERALLY CHAPTER 1--ORGANIZATION Sec. 105. Executive agencyFor the purpose of this title, ``Executive agency'' means an Executive department, a Government corporation, and an independent establishment. Pub. L. 89-554, Sept. 6, 1966, 80 Stat. 379.) Historical and Revision Notes The section is supplied to avoid the necessity for defining ``Executive agency'' each time it is used in this title.

5 U.S.C. §101: Executive Departments

TITLE 5 > PART I > CHAPTER 1 > § 101

The Executive departments are:

The Department of State.

The Department of the Treasury.

The Department of Defense.

The Department of Justice.

The Department of the Interior.

The Department of Agriculture.

The Department of Commerce.

The Department of Labor.

The Department of Housing and Urban Development.

The Department of Transportation.

The Department of Energy.

The Department of Education.

The Department of Veterans Affairs.

5 U.S.C. §104: Independent Establishment

TITLE 5 > PART I > CHAPTER 1 > § 104

§ 104. Independent establishment

For the purpose of this title, “independent establishment” means—

(1) an establishment in the executive branch (other than the United States Postal Service or the Postal Rate Commission) which is not an Executive department, military department, Government corporation, or part thereof, or part of an independent establishment; and

(2) the Government Accountability Office.

5 U.S.C. §103: Government Corporation

TITLE 5 > PART I > CHAPTER 1 > § 103

For the purpose of this title—

(1) “Government corporation” means a corporation owned or controlled by the Government of the United States; and

(2) “Government controlled corporation” does not include a corporation owned by the Government of the United States.

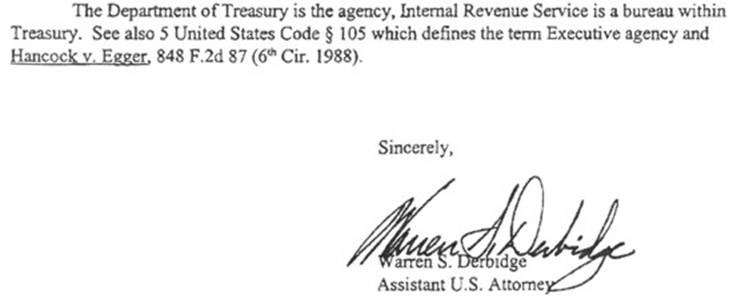

U.S. Attorney Warren Derbridge's definition of the IRS

Hancock v. Egger, 848 F.2d 87 (6th Cir. 1988)

Section 2000e-16(c) of Title 42 mandates who may be a proper defendant in civil actions brought by federal employees to enforce rights under Title VII of the Civil Rights Act of 1964, as amended, the Equal Employment Opportunity Act of 1972. That section provides that "the head of the department, agency, or unit, as appropriate, shall be the defendant." (emphasis added). For the Commissioner of the Internal Revenue Service to be a proper defendant, therefore, we would have to conclude that the Internal Revenue Service is either a "department," "agency," or "unit." Resolution of this issue is purely a question of statutory interpretation.

The terms "department," "agency," and "unit," found in § 2000e-16(c), are defined in subsection (a) of § 2000e-16. Congress clearly intended these definitions found in subsection (a) to be incorporated into the mandatory requirements of subsection (c). Accordingly, "department" is defined in subsection (a) as "military departments as defined in § 102 of Title V." Certainly, the Internal Revenue Service does not fit within the definition of a military department. In subsection (a), "unit" is defined as "those units of the Government of the District of Columbia having positions in the competitive service, and . . . those units of the legislative and judicial branches of the Federal Government having positions in the competitive service." It is without question that the Internal Revenue Service does not fit this definition and, therefore, cannot be characterized as a "unit."

Plaintiff's only remaining recourse is to argue that the Internal Revenue Service is an "agency" within the meaning of§ 2000e-16(c). This term is defined, however, in subsection (a) as "executive agencies as defined in § 105 of Title V." "Executive agencies" are defined in 5 U.S.C. § 105 (1970) as "an Executive Department, a Government corporation, [or] an independent establishment." Only if the Internal Revenue Service qualifies as an "executive department," a "government corporation" or an "independent establishment" can it be defined as an "agency" within the meaning of subsection (a) of § 2000e-16. Section 101 of 5 U.S.C. (1970) defines "Executive department" by listing the eleven cabinet-level departments. While the Department of the Treasury is listed, the Internal Revenue Service is not. Thus, the Internal Revenue Service is not an "executive department." Section 104 of 5 U.S.C. (1970) defines "independent establishment" as "an establishment in the executive branch . . . which is not an Executive Department, Military Department, Government Corporation, or part thereof . . . ." Because the Internal Revenue Service is clearly a part of an executive department, the Department of Treasury, the Internal Revenue Service does not meet the definition of an "independent establishment." Finally, it is not and cannot be alleged that the Internal Revenue Service is a government corporation within the meaning of 5 U.S.C. § 105. Thus, the Internal Revenue Service is not an "agency" for the purpose of § 2000e-16.

On the basis of our analysis of the statutory language, which analysis parallels that of Stephenson v. Simon, 427 F. Supp. 467 (D. D.C. 1976), we conclude that plaintiff incorrectly named the Commissioner of the Internal Revenue Service as a defendant in this employment action. The only proper defendants in such actions are the heads of a "department, agency, or a unit" within the meaning of § 2000e-16. The proper defendant was not named in this action. Adherence to the statute's requirements is mandatory, and we are neither authorized nor inclined to ignore its mandate.

[Hancock v. Egger, 848 F.2d 87 (6th Cir. 1988)]

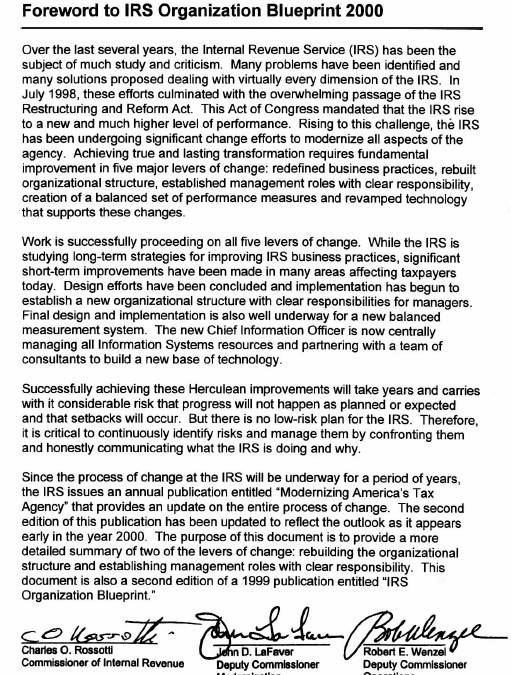

Modernizing

Americas Tax Agency: IRS Organizational Blueprint, p. 3 of 276, Charles

Rosotti, Commissioner of the IRS

T. Coleman Andrews, in a

June 18, 1953 Memorandum

to George W. Humphrey, the

Secretary of the Treasury,

wrote the following:

“It seems to me that there is some real practical psychological value to be derived from the substitution of the word ‘Service’ for ‘Bureau’. The name ‘Bureau of Internal Revenue’ is not a name created by statute, but has been adopted by usage… The Act of July 1, 1862 [12 Stat 432] which is generally understood to be the foundation of the present Internal Revenue system…”

Internal Revenue Service:

The current name of the “Bureau of Internal Revenue” (BIR) of Puerto Rico. The “Federal Alcohol Administration” created on 8-29-1935, 49 Stat. 977; 27 USC § 201, was abolished and absorbed in the BIR on 4-2-1940 by Reorganization Plan No. III of 1940, 5 F.R. (Federal Register) 2107, 54 Stat. 1232, set out in the Appendix to Title 5, Government Organization and Employees. Department of the Treasury Order (TDO) 221 of July 1, 1972, established the BATF and transferred to it the alcohol and functions of the Internal Revenue Service. Public law 97-258 §5(b), Sept 13, 1982, 96 Stat. 1068, 1085 repealed §2 of the 1940 Reorganization Plan No III and the first section of which enacted Title 31, Money and Finance. Reference: US Statues at Large and 27 USC §201