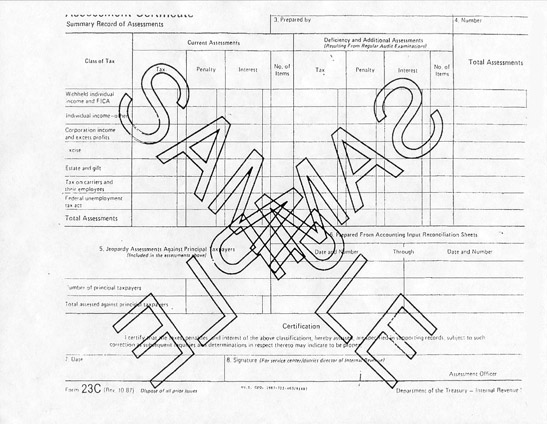

23C Assessment Forms

Certificate

Internal Revenue Manual 3

Internal Revenue Manual 3(17)(63)(14).1 |

Account 6110 Tax Assessments

(2) All tax assessments must be recorded on Form 23C Assessment Certificate. The Assessment Certificate must be signed by the Assessment Officer and dated. The Assessment Certificate is the legal document that permits collection activity…

Internal Revenue Manual 3(17)(46)2.3 |

Certification

(1) All assessments must be certified by signature of an authorized official on Form 23-C, Assessment Certificate. A signed Form 23C authorizes issuance of notices and other collection action…

(2) Some assessments are prescribed for expeditious action as and be certified on a daily basis. These assessments will require immediate preparation of Form 23C from RACS…

Form 23C is described in Document 7130, IRS Printed Product Catalog as:

23C - Assessment Certificate-Summary Record of Assessments

Form 23C is used to official assess tax liabilities. The completed form is retained in the Service Center case file as a legal document to support the assessment made against the taxpayer. This status notice is reissued to update the status notice file. TR:R:A Internal Use |

Court Case

CURLEY v. U.S.

Cite as 791 F. Supp 52 (E.D.N.Y. 1992)

… [5] Plaintiff relies heavily on Brafman v. United States, 384 F.2d 863 (5th Cir. 1967), where an assessment was invalidated due to the lack of a signature on the 23C Form. This defect, however, was a significant violation of the regulation…

…A signature requirement protects the taxpayer by ensuring that a responsible officer has approved the assessment…

764 FEDERAL SUPPLEMENT Page 315

BREWER v. U.S.

Cite as 764 F.Supp. 309 (S.D.N.Y. 1991)

…However, there is no indication in the record before us that the "Summary Report of Assessments", known as Form 23C, was completed and signed by the assessment officer as required by 26 C.F.R. § 301.6203-1.3 Nor do the Certificates of Assessments and Payments contain 23C dates which would allow us to conclude that a Form 23C form was signed on that date. See United States v. Dixon, 672 F. Supp. 503, 505-506 (M.D.Ala.1987). Thus we find that the plaintiff has raised a factual question concerning whether IRS procedures were followed in making the assessments…

3 This regulation provides, in relevant part, that "[t]he assessment shall be made by an assessment officer signing the summary record of assessment…